Across Europe, the notion of ‘home’ has become increasingly fraught. In the past decade, property values have ballooned by more than 60%, rents have crept up by 20%, and nearly one in six Europeans wrestles with overcrowded or inadequate housing, while roughly a million have no shelter at all. The housing landscape is scarred by a succession of shocks: pandemic-era savings surges, energy-price turbulence, and migration-driven demographic shifts collide with a supply side hampered by soaring material costs, labour scarcities, and labyrinthine bureaucracy. Policymakers scramble to marshal billions, streamline planning, and accelerate innovative construction, confronting a choice between fragmented, reactive measures or a cohesive, continent-spanning strategy that could transform housing from a source of anxiety into a bedrock of social and economic cohesion.

Spurred by soaring prices and mounting concerns over affordability, the team at RationalFX analysed the European housing market through multiple lenses: patterns of ownership, the distribution of dwelling types, and price trends both per home and per square metre, alongside year-on-year changes. We also mapped the largest markets, assessed construction output relative to population, and explored regional disparities, aiming to reveal the structural forces and imbalances that shape where and how Europeans live today.

Key Takeaways:

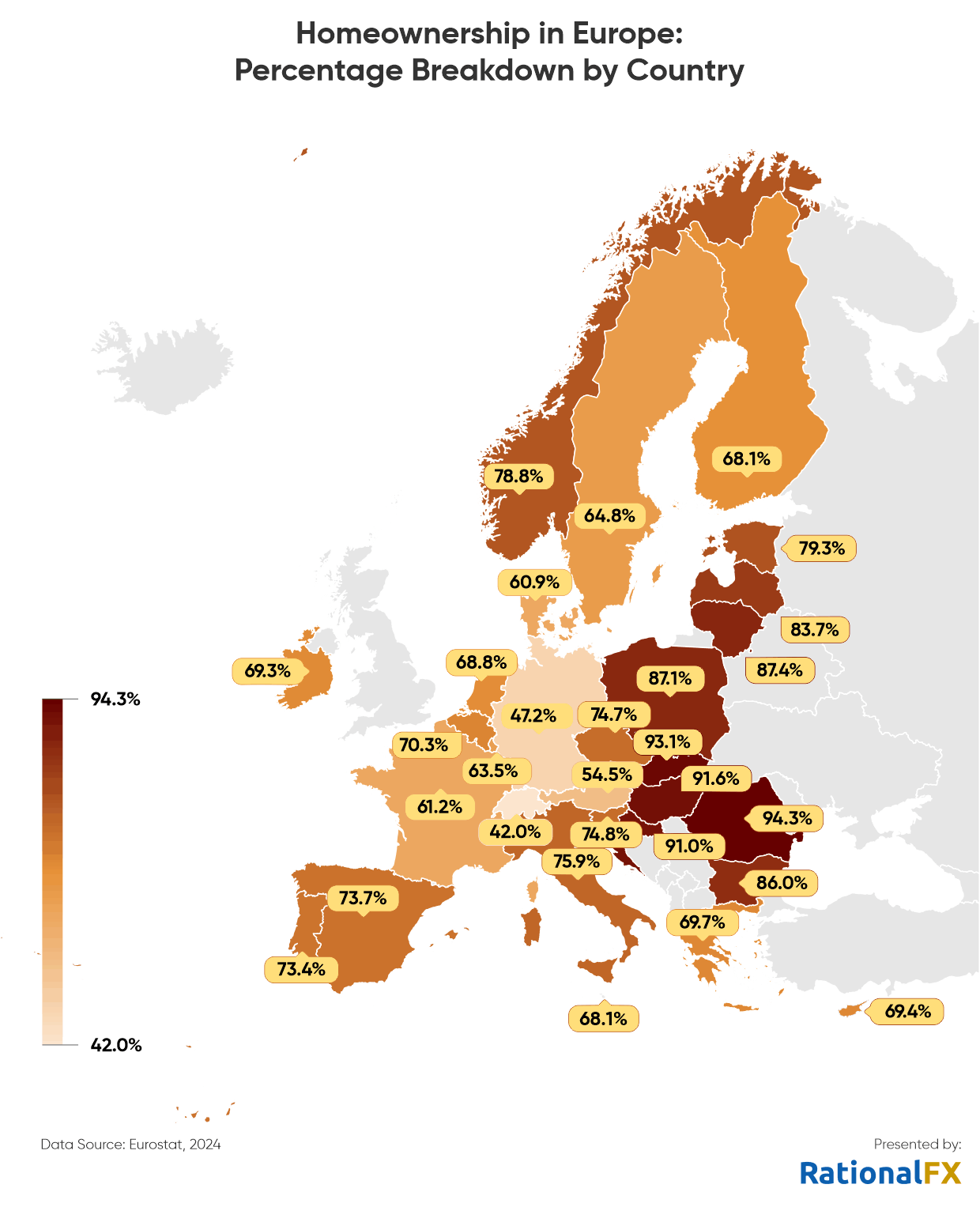

- Romania, Slovakia, Hungary, and Croatia have the highest homeownership rates, with over 90% of their populations owning their homes.

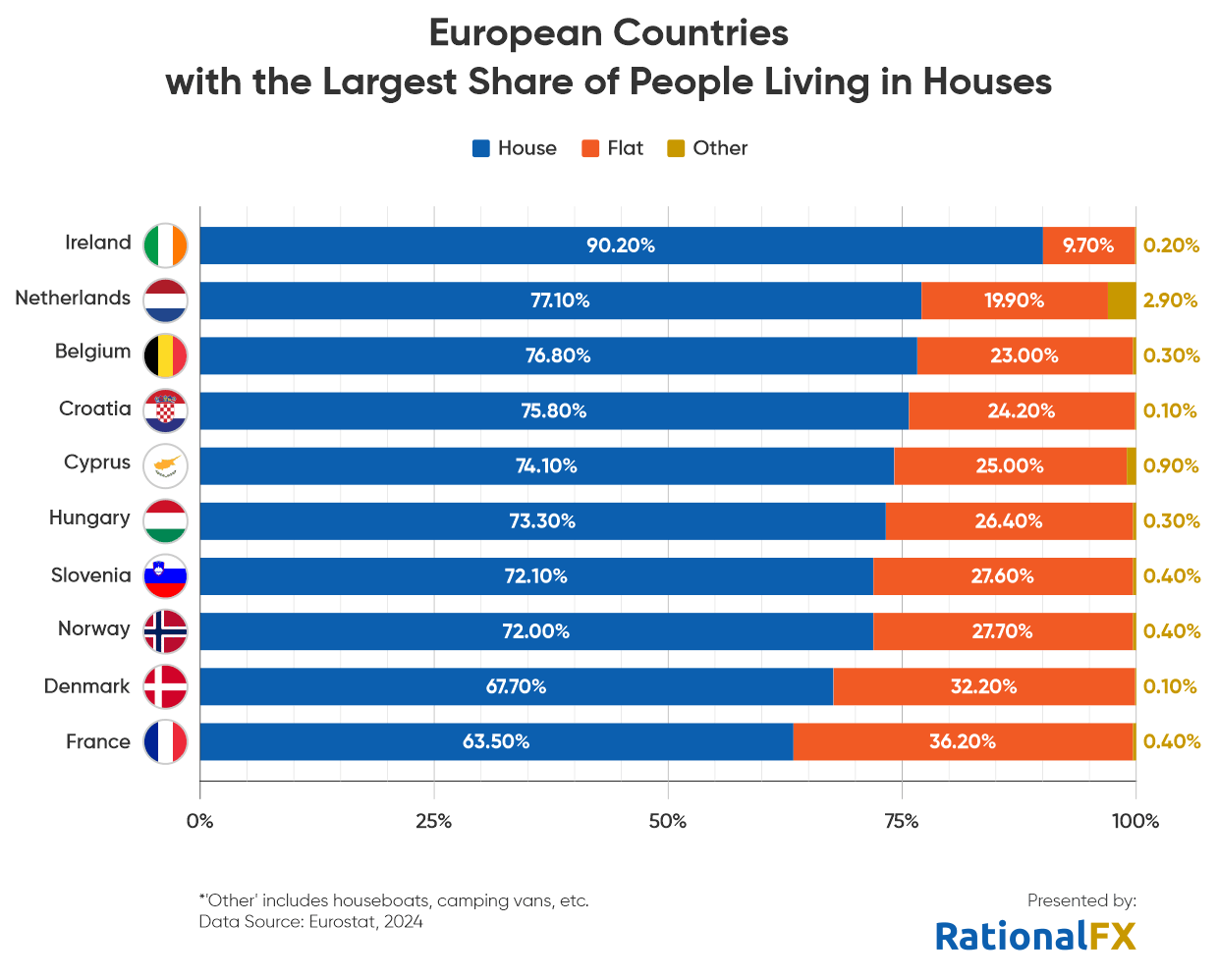

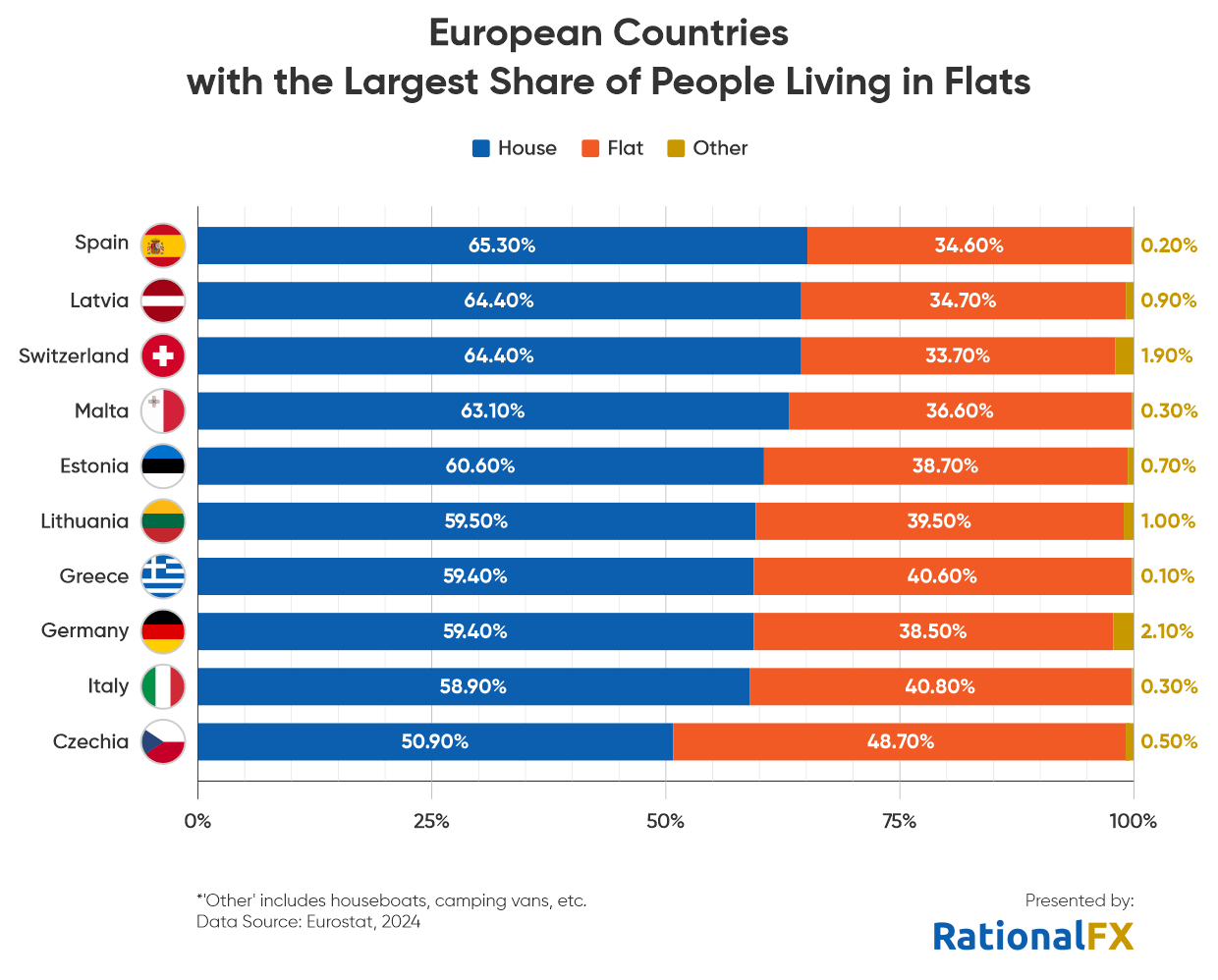

- Houses are the most common type of dwelling in Ireland (90%) and the Netherlands (77%), whereas apartments are more prevalent in Spain (65%), Latvia (64%), and Switzerland (64%).

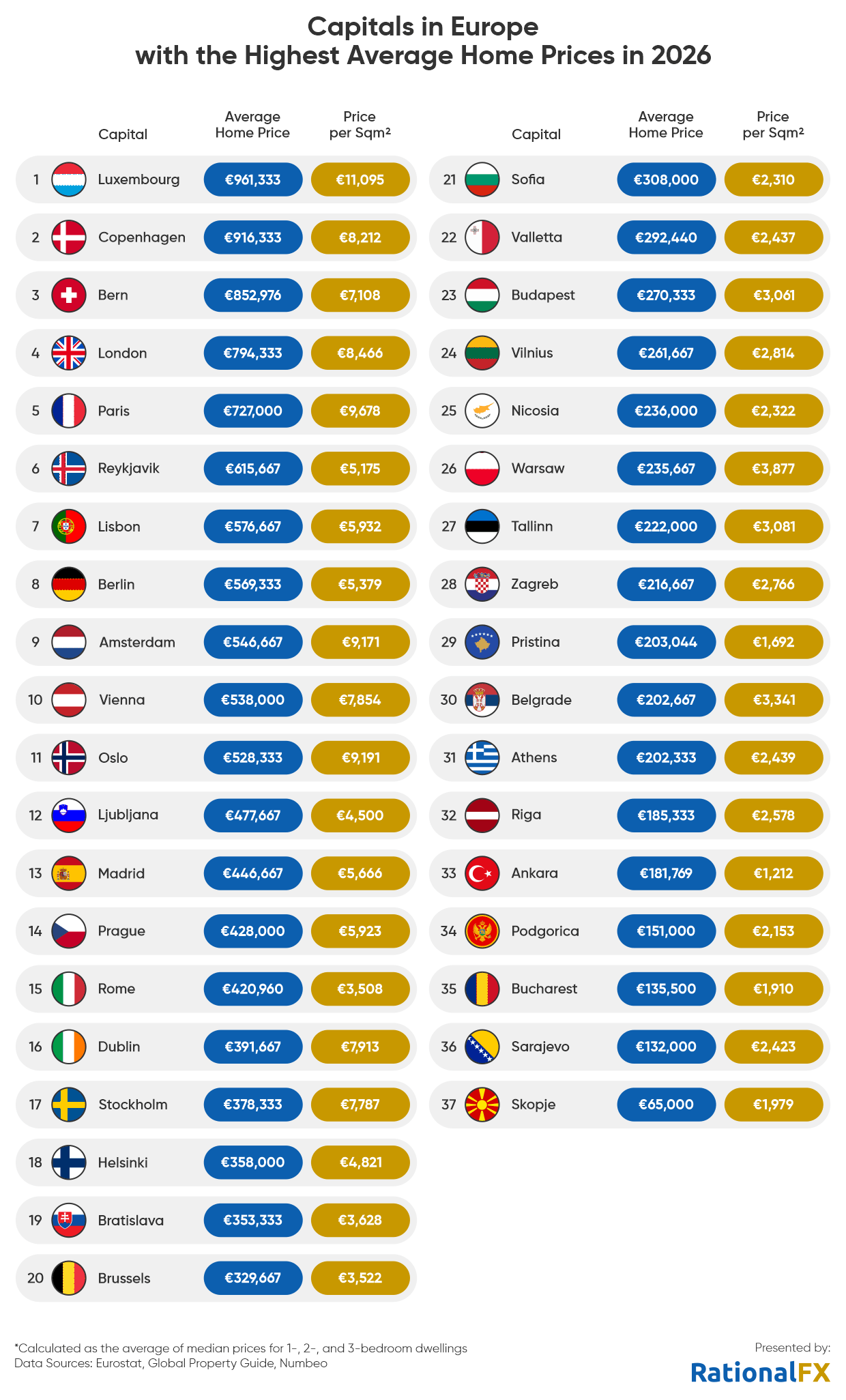

- The priciest capitals for average homes are Luxembourg and Copenhagen, both exceeding €900,000; per-square-metre prices are highest in Luxembourg (€11,095), followed by Paris (€8,212) and Oslo (€7,108).

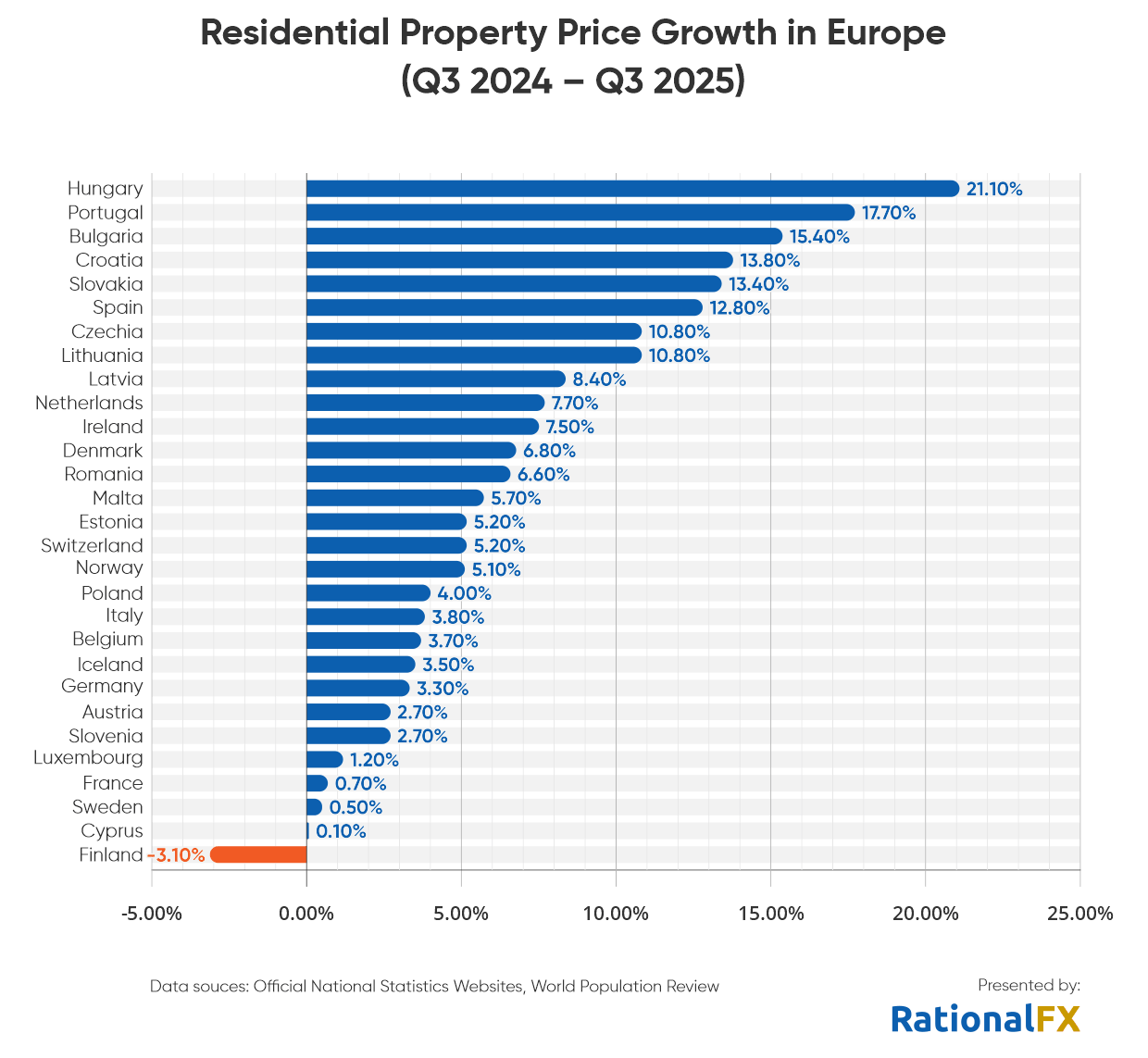

- Between 2024 and 2025, property prices surged most in Hungary (+21%), Portugal (+18%), and Bulgaria (+15%).

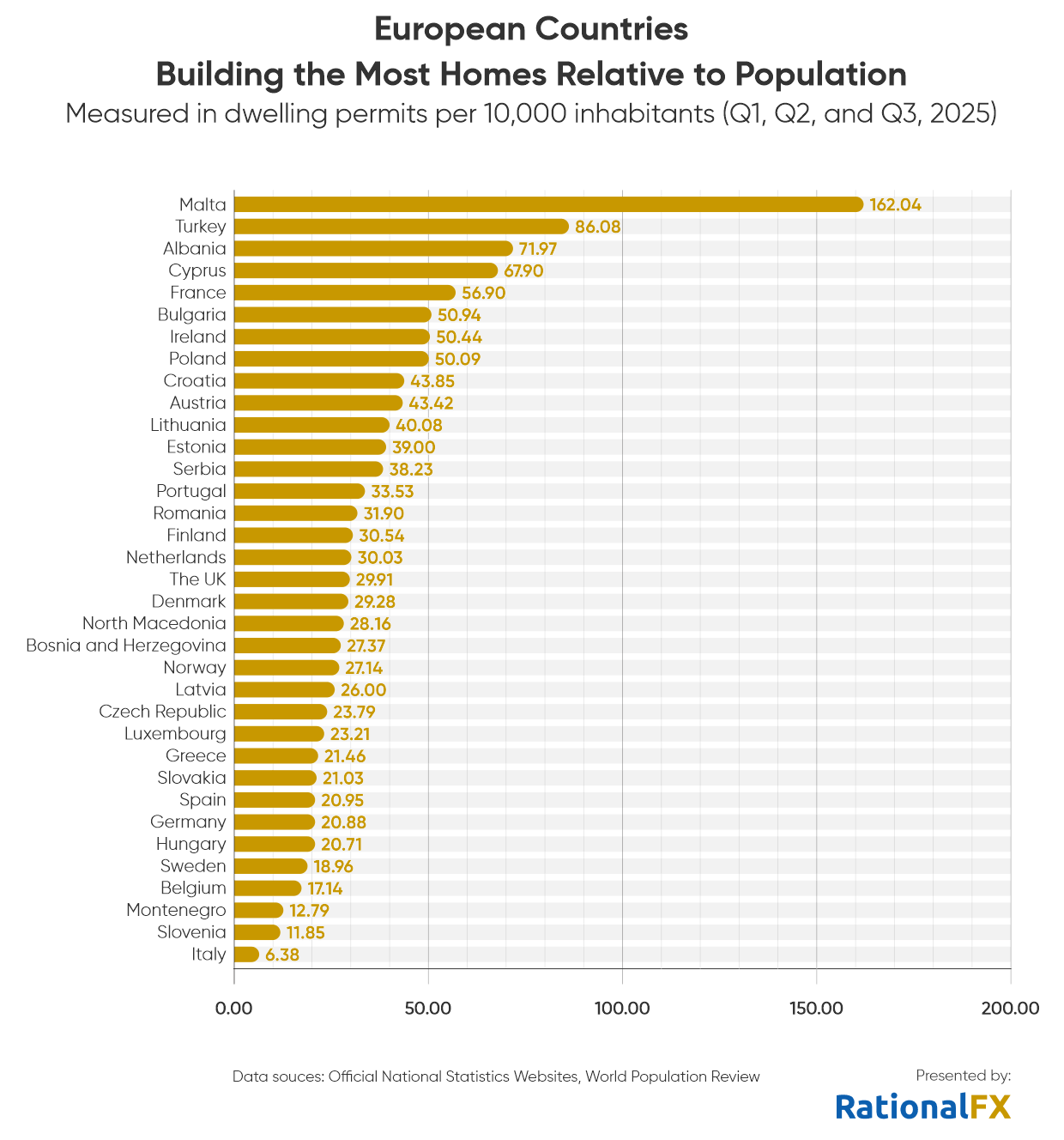

- Relative to population, Malta leads in new construction with 162 new dwelling permits per 10,000 residents, followed by Turkey with 86 and Albania with 72.

Holding the Keys, But at What Cost? Exploring Europe’s Shifting Housing Landscape

Owning a home in Europe has grown ever more elusive, as rising prices, regulatory complexity, and urban density reshape the very concept of dwelling. In Romania (94.3%), Slovakia (93.1%), Hungary (91.6%), and Croatia (91%), the vast majority still held the keys to their homes in 2024, reflecting historical land legacies and enduring cultural habits. Yet even in these markets, central urban areas are seeing affordability erode, mortgage conditions tighten, and younger generations increasingly reliant on inherited properties. This suggests that while headline ownership rates remain high, true accessibility is waning, hinting at a slow but steady shift toward concentrated property control and the potential redefinition of homeownership across Europe.

Southern Europe – Italy (75.9%), Spain (73.7%), Portugal (73.4%) – retains relatively high ownership, whereas in Austria (54.5%), Germany (47.2%), and Switzerland (42%) renting predominates, underpinned by strong tenant protections, extensive social and cooperative housing, and stable long‑term rental frameworks that render renting a more secure and common choice rather than a fallback.

The Shape of Home: Distribution of Houses and Apartments Across Europe

Across Europe, the choice of dwelling is more than a matter of square footage – it is a window into culture, history, and economic reality. In some corners, sprawling homes dominate, echoing rural traditions and familial legacies; in others, vertical living prevails, shaped by soaring city skylines, planning constraints, and the rising cost of modern life. This distribution of dwellings reveals not just where people live, but how they live – and how much they are willing or able to invest in the spaces they call home.

The predominance of houses in countries such as Ireland (90.2%), the Netherlands (77.1%) and Belgium (76.8%) reflects both longstanding residential traditions and acute market pressures. In Ireland, where a majority of the population lives in rural or suburban areas, house price inflation has remained persistently high, with average home prices continuing to rise in 2025. In the Netherlands and Belgium, while urbanisation is higher, similar pressures – constrained space, rising prices, and planning restrictions – contribute to the continued dominance of houses over apartments, though market dynamics vary regionally.

Meanwhile, the Dutch and Belgian markets, despite strong policy efforts to increase overall housing supply, still see houses dominate because new construction has lagged behind demographic growth, and affordability constraints make inner-city living – and smaller flats – less accessible for many families.

Apartment living dominates in parts of Europe where housing demand has outpaced the ability to expand outward, forcing cities to grow upward instead. In Spain, where over two-thirds of residents live in flats, demand remains buoyant as foreign buyers purchased almost 100,000 homes in 2025 – the highest level since the pre-financial-crisis boom – intensifying competition in already dense urban markets.

Switzerland and Germany’s strong apartment presence reflects a housing landscape shaped less by necessity than by institutional stability, where renting and multi-unit living are deeply embedded in urban planning and financial structures. In Berlin, however, years of stalled construction, slow permitting, and rising costs have left demand far exceeding supply, creating long queues for viewings and soaring rents, despite government efforts to accelerate development through ‘construction turbo’ laws.

In Malta and Greece, a large share of residents still live in apartments that date back to the post‑World War II building boom, many of which are now undergoing gradual modernisation. In Malta, projects such as the $40 million development in Malta town signal efforts to expand contemporary rental options, while in Greece, decades of halted construction, soaring rents, and foreign property investment have increasingly displaced middle-class residents from city centres.

Europe’s Most Expensive Capitals to Buy a Home in 2026: Booming Cities with Sky-High Prices

Luxembourg City reigns supreme not only in average home price (€961,333) but also in per‑metre valuation, exceeding €11,000/m², and rental rates among the highest in Europe, driven by tight supply, strong labour inflows, and limited land availability. Copenhagen and Bern follow, with their elevated average home prices of between €852,976 and €916,333, reflecting wealthy labour markets and entrenched demand for premium urban addresses. London and Paris remain perennial outliers in the Western hierarchy, where total purchase prices combine large unit sizes with sky‑high per‑square‑metre premiums amid ongoing affordability debates and slowing mortgage markets.

On the more affordable end, Skopje (€65,000) stands out as Europe’s cheapest capital for home purchasing – less than half the price of the next cheapest cities, Sarajevo (€132,000) and Bucharest (€135,500). These lower price levels reflect slower economic growth, weaker incomes, and minimal foreign demand. Yet Sofia (€308,000) bucks the Eastern trend, approaching Brussels (€330,000), with prices continuing to surge in 2026, following Bulgaria’s adoption of the euro and rising local demand.

The New Geography of Housing Price Growth

Between Q3 2024 and Q3 2025, Europe’s housing markets traced a striking divergence rather than uniform acceleration, revealing deep structural contrasts across the continent. At the sharp end, Hungary’s residential prices leapt over 21%, followed by Portugal (+17.7%) and Bulgaria (+15.4%), all far above the EU average of roughly 5.5%, as demand outstripped supply and investor interest remained robust.

Portugal’s market, long flagged by the European Commission as among the most overvalued in the euro area, continues to feel pressure from foreign buyers and slow construction rates, while Bulgaria’s dynamic growth highlights the allure of lower‑cost capitals on the cusp of macroeconomic transition. Croatia, Slovakia and Spain likewise posted double‑digit gains, driven by income growth, limited new builds and renewed migration into urban centres.

By contrast, established Western and Nordic markets exhibited subdued momentum: Luxembourg, France and Sweden hovered near flat growth, and Finland even recorded a contraction – a testament to how mature price landscapes and demographic stagnation can temper housing demand even as overall European prices climb.

This uneven tapestry of change indicates that by early 2026, the pace of price growth is being shaped not by simple regional patterns but by deeper market mechanics: where supply remains constrained and financing conditions shift, prices accelerate; where stock is abundant, and credit tightens, growth plateaus. In such a context, capital flows – both domestic and cross‑border – and differentiated confidence in local economies are steadily recasting traditional hierarchies in Europe’s housing markets, with implications for affordability, investment strategy, and policy calibration over the coming cycle.

The European Nations Leading the Housing Boom

Construction in Malta – 8,838 dwellings permitted in the first nine months of 2025 or an average of 162 permits per 10,000 residents – continues to be driven by foreign investment and domestic population growth. Acquisition of Immovable Property (AIP) permits issued to non-EU citizens have more than doubled since 2021, with Chinese buyers alone accounting for roughly 40% of all such permits between 2021 and 2025, exacerbating affordability pressures even as the Central Bank of Malta notes that prices are gradually correcting after a decade of steep growth.

Albania and France follow, with 86 and 72 new dwellings permitted per 10,000 inhabitants, respectively. Albania is experiencing a surge of high-profile projects, many by internationally renowned architects, reshaping the skylines of Tirana and other urban centres. By contrast, France saw construction volumes decline by 1.5% in 2025, with sector confidence remaining subdued, despite ongoing GDP growth. Ireland ranks fourth, with 68 new dwellings permitted per 10,000 inhabitants, as the government pursues an ambitious target of 300,000 new homes by 2030.

Turkey dominates in absolute terms, issuing 754,791 dwelling permits between January and September 2025 – more than twice the volume of France and the United Kingdom combined. This unprecedented output reflects the combined pressures of post-earthquake reconstruction, rapid urban expansion, and government-backed housing initiatives aimed at addressing long-standing supply constraints.

Methodology

Residential construction and affordability across Europe were assessed using a combination of official and publicly available sources for 2024-2025. Homeownership rates and the most common dwelling types (2024), along with year-on-year changes in dwelling prices (Q3 2024-Q3 2025), were sourced from Eurostat. Average home prices by dwelling size and price per square metre were taken from Global Property Guide, with Numbeo used to fill any gaps.

Data on building permits and new dwellings approved in the first three quarters of 2025 were collected from national statistical offices or government sources. These totals were then adjusted for population (2025 estimates from World Population Review) to calculate new dwellings permitted per 10,000 inhabitants, enabling comparable assessments of construction activity, supply dynamics, and affordability pressures across countries.